Urbanisation 2.0

La popolazione urbana mondiale attualmente rappresenta il 55% del totale. Nonostante la pandemia di COVID-19 abbia rallentato questa tendenza all’urbanizzazione, le Nazioni Unite si aspettano un progressivo aumento delle megalopoli, ossia città con più di 10 milioni di abitanti, da 31 nel 2018 a 43 nel 2030, e stimano una percentuale di abitanti a livello mondiale nelle città pari al 66% nel 2050.

Leggi l'articolo in inglese

Urbanisation 2.0

Global urban population represents currently the 55% of the total. The COVID-19 pandemic shifted some urban dynamics (working from home, lifestyle & commuting) leading suburbs growing faster than urban areas. However, the overall urbanisation trend is expected to keep growing. The United Nations expects an increase in the number of megacities, cities with more than 10 million residents, to 43 (vs 31 in 2018) by 2030 and the 66% of the global population living in cities by 2050.

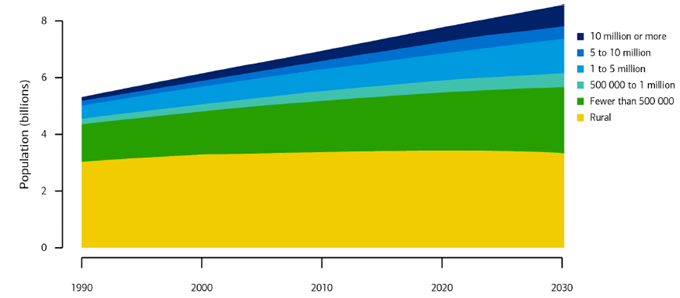

According to BoFA Global Research, about 752 million people or more are expected to live in urban areas by 2030, representing 8.8% of the global population.

source: Bank of America (“BoFA”)

According to PwC, this process of urbanisation will lead to an increase of the investments in infrastructure, which are expected to cost up to $78trn over the next 10 years. Urbanisation will not increase uniformly globally since its growth will majorly be driven by Africa and Asia. This process is environmentally risky due to the possibility of leading to congestion and pollution phenomena, which are typical of large urban areas.

The possible solutions to avoid, or at least mitigate, these risks are the following:

- Investment in infrastructure

- Significant public spending on social amenities

- Improvement of waste management

- Increase in clean mobility

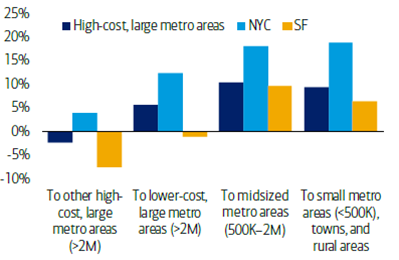

At the peak of COVID, in the US there has been an urban exodus driven by the possibility to work from home. Thanks to smart working, people have started looking for larger and more affordable houses outside urban areas, but post COVID, US cities are expected to recover. According to latest data, rents in all major markets had recovered and reached higher levels than pre-pandemic ones.

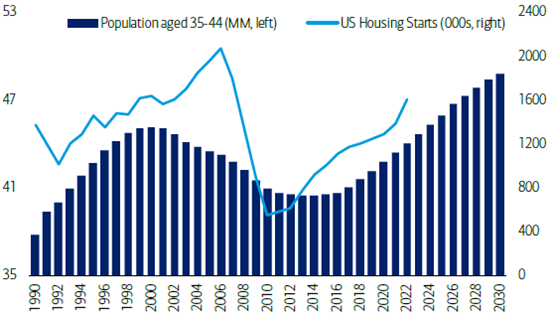

An additional favorable demographic trend that will likely benefit urban growth is led by Millennials since this generation is now the biggest demographic group in the US, being in their prime home-buying years.

Estimates (% change) migration from large metro areas to other regions during the Pandemic

(source: BoFA Global Research)

Increasing amount of 35–44-year-olds in the US should be favorable for housing starts

(source: BoFA Global Research)

In conclusion, urbanisation trend will remain strong, and it will keep growing, especially in emerging markets. However, COVID has changed the landscape in some regions (like the US) through work-from-home options and immigration to suburbs to avoid high-cost cities.

According to Bofa Global Research, Asia and Africa urbanisation rates are expected to catch up by 2050. The sharp increase in population and immigration from rural to urban areas will drive the pace of urbanisation growth in these two regions. Africa’s urbanisation rate was 43% in 2018 but it is projected to grow to 59% in 2050, while Asia is estimated to have the largest number of urban inhabitants at 3.5 billion. The process of urbanisation in Asia is strongly linked to the economic transition and the greater integration into the global economy, mainly in the form of the outsourcing of manufacturing of consumer goods by parent companies in developed countries.

Levels of urbanization in 1980, 2015 and projections to 2050. Africa’s level or urbanization in 2050 to be 2x of the 1980s

(source: BofA securities; United Nations (2018d), World Urbanization Prospects: The 2018 Revision)

Disclaimer:

Nothing in this document is intended as investment research or as a marketing communication, nor as a recommendation or suggestion, express or implied, with respect to an investment strategy concerning the financial instruments managed or issued by Eurizon Capital SGR S.p.A.. Neither is this document a solicitation or offer, investment, legal, tax or other advice.

The opinions, forecasts or estimates contained herein are made with reference only to the date of preparation, and there can be no assurance that results or any future events will be consistent with the opinions, forecasts or estimates contained herein. The information provided and opinions contained are based on sources believed to be reliable and in good faith. However, no representation or warranty, express or implied, is made by Eurizon Capital SGR S.p.A. as to the accuracy, completeness or fairness of the information provided.

Any information contained in the present document may, after the date of its preparation, be subject to modification or updating.